Section 26 Correlation

Correlation

It is a measure of association between continuous variables

Karl Pearson developed the correlation coefficient from a similar but slightly different idea by Francis Galton

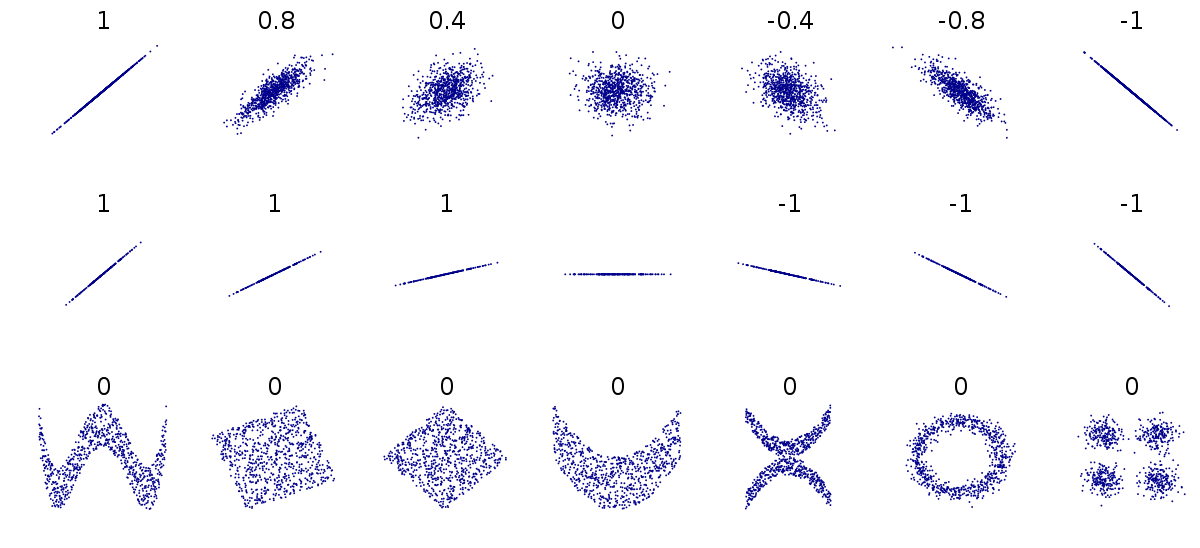

It only applies to the linear relationship

The estimate of correlation lies between -1 and +1 - Values less than zero imply negative correlation - Values greater than zero imply positive correlation - Values close to 1 or -1 imply strong correlation - Values close to 0 imply little or no correlation

Correlation does NOT imply causation

Rank correlation coefficients, such as Spearman’s rank correlation coefficient and Kendall’s rank correlation coefficient, measure the association of two variables without a linear relationship condition.

Note that correlations are symmetric in the sense that r(x,y) = r(y,x).

Formula of correlation: Uses covariance and variance of two variables x & y

Centering and Scaling of the data x & y

Formula of Correlation Coefficient

\[ \large r_{xy} = \frac{Cov(x,y)}{\sqrt{(Var(x)Var(y)}} = \frac{Cov(x,y)}{s_xs_y} \]

\[ \large Cov(x,y) = s_{xy} = \frac{1}{n-1}\sum\limits_{i=1}^{n} (x_i-\bar{x})(y_i-\bar{y}) \]

\[ \large Var(x) = s_x^2 = \frac{1}{n-1}\sum\limits_{i=1}^{n} (x_i-\bar{x})^2 \]

\[ \large Var(y) = s_y^2 = \frac{1}{n-1}\sum\limits_{i=1}^{n} (y_i-\bar{y})^2 \]